An action tank for the democratisation of wealth

3 Policies to Support Informal Workers to Save for a Pension

If the global retirement landscape does not change, over two billion people in the world today will retire without access to a pension. Many will have worked in the informal sector (i.e. operating outside of formal employment arrangements and related pension systems) which globally now constitutes more of the global labour force than the formal employment sector.

In many low- and middle-income countries, less than 1% of informal workers have pension accounts. This is a problem not only because it leaves individuals risking poverty in old age, but it also creates a slow-burn financial crisis with under-funded pensions systems unable to cover an ageing global population.

Our recent research report, in collaboration with D3P Global, looked at this problem in detail and assessed the initiatives tried in 11 emerging markets and developing economies to boost participation in pensions among informal workers. You can read the full report (or summary version) here, but in this blog we summarise three of the most promising innovations highlighted in the report:

1. Save for your pension, get free insurance

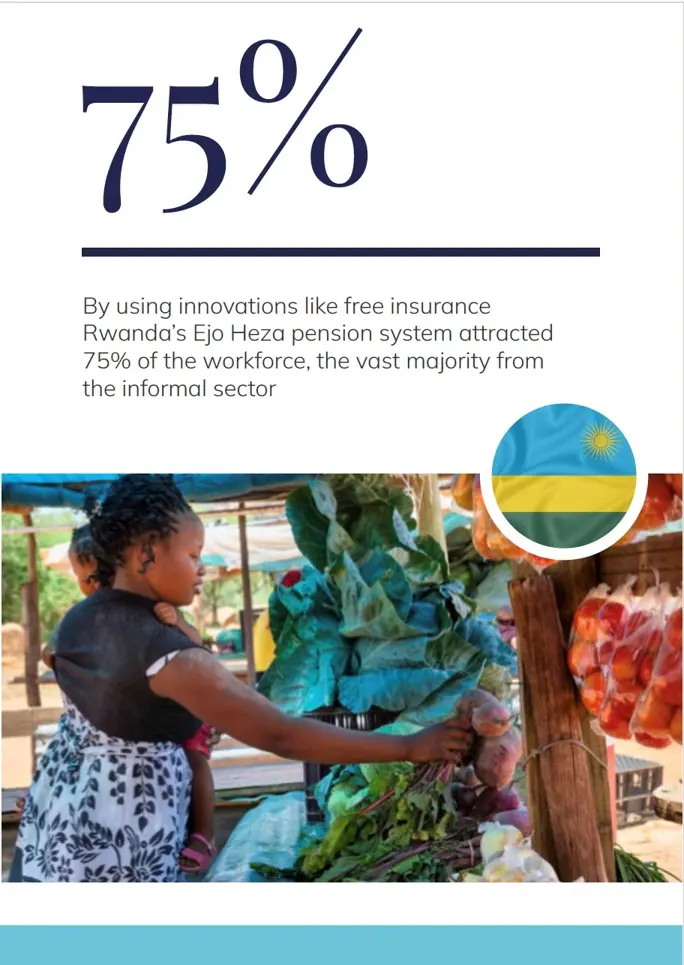

Rwanda’s ‘Ejo Heza’ plan for informal workers was introduced in 2018 and has seen world-leading results by encouraging 3.2 million workers to open accounts. A key innovation is the inclusion of funeral insurance – a crucial product in Rwanda given rising burial costs – alongside other benefits such as matching contributions and flexible withdrawal terms.

The ‘bundled products’ approach merits consideration in other countries. For some workers ‘free’ life, health or accident insurance may motivate them to take out a pension. Even if insurance is not bundled in the pension plan, access to (micro) insurance is important to give informal workers the confidence they can save some money longer term in a pension rather than needing cash to fund a medical emergency in their own or extended family.

2. Auto enrolment, even when there’s no formal employer

The introduction of auto-enrolment, where employees automatically contribute to a pension scheme unless they consciously opt-out, has been a powerful way of boosting pension participation in the formal sector. In the UK for example, the share of employees with workplace pensions increased from around 50% to nearly 80%, in eight years following the introduction of auto-enrolment.

Auto-enrolment via employers however, cannot, by definition, work for the informal labour force who lack a formal work contract. Yet some developing countries in Africa have adapted the mechanism for informal workers.

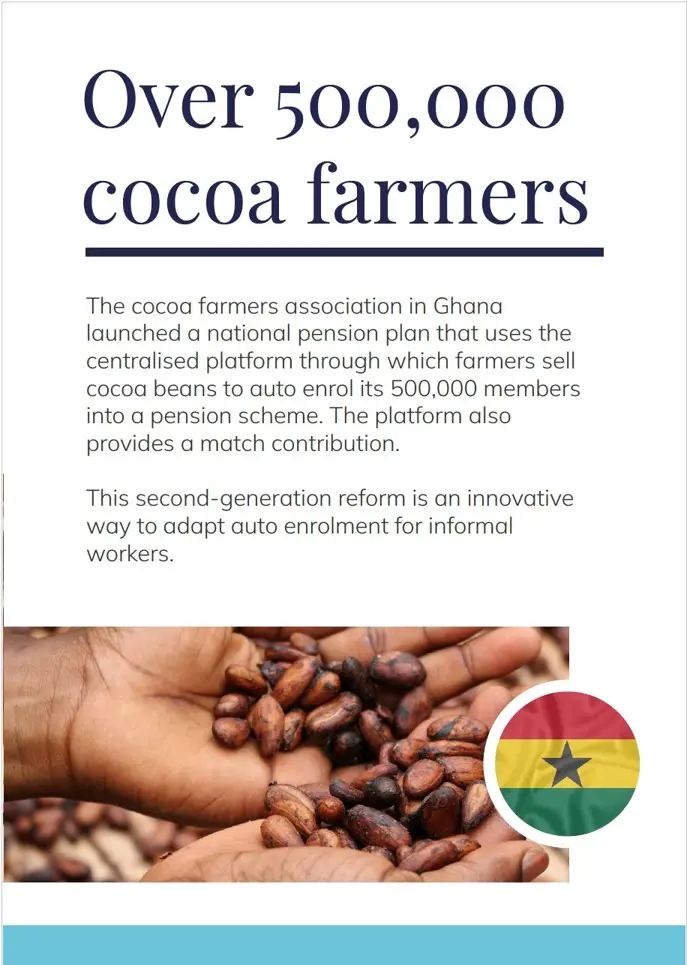

In Ghana, the Ghana Cocoa Board (COCOBOD) launched a national pension plan for over 500,000 farmers that leverages the centralised system those farmers use for selling cocoa beans. The plan automatically diverts 5% of a farmer’s sales from the centralised purchasing arrangements into a pension plan – with farmers receiving a 20% match from the cocoa board. A similar innovation that we label ‘second generation auto-enrolment’, has been seen in Kenya in combination with a youth empowerment programme. ‘Second generation auto-enrolment’ are initiatives that leverage auto-enrolment through an institution that gathers a large group of workers, but is not their employer.

3. Generous matching contributions and targeting low-income women

Matching contributions means the government (or employer or other entity) adds extra money when the worker pays into their pension scheme. It is widely seen as one of the most effective ways of incentivising participation for informal sector workers.

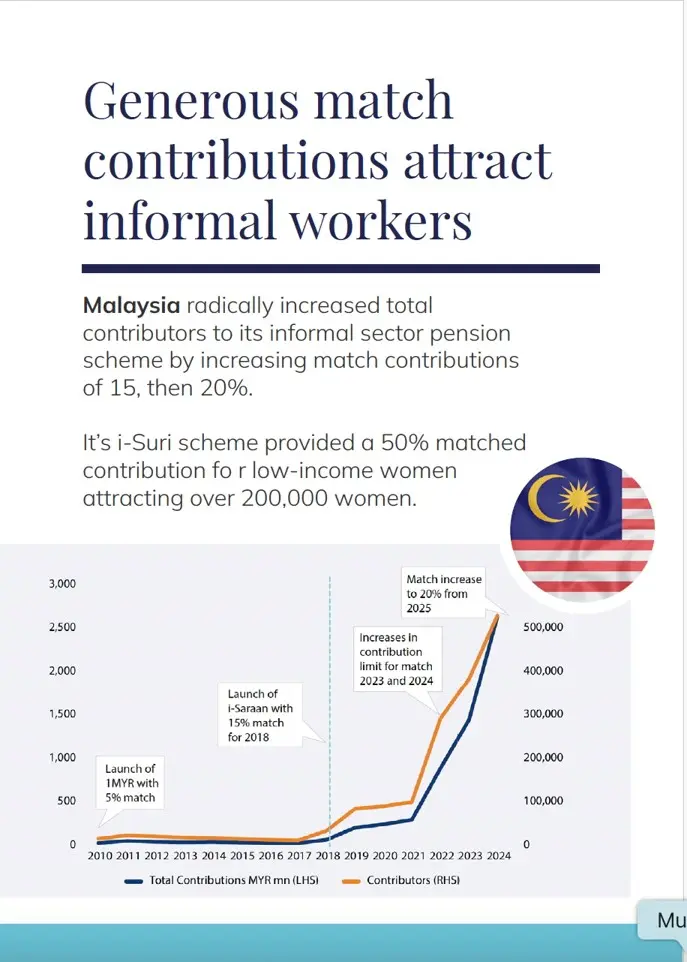

In Malaysia, a pension plan for the informal sector (launched in 2010) was revamped in 2018 to offer matching contributions of 15% (increased to 20% in 2025). Participation rocketed to 529,000 accounts by end 2024, which has played a role in extending pension coverage to up to 15% of the informal sector. This was a dramatic increase on the initial 2010 scheme which only had a 5% match.

Another innovation in Malaysia that is worth highlighting is the i-Suri scheme, launched in 2018, which provided a 50% matched contribution for low-income married women registered in the Government’s poverty database. This initiative saw accounts grow strongly to over 200,000 women. The plan showed what is possible in terms of targeting if the systems exist to link pension plans and match savers to other government databases – a tactic also employed by Rwanda’s Ejo Heza system.

No silver bullet

While all three ideas are strong, another clear message from our full research, was that there is no one size first all approach to increasing informal sector pension participation. Even the most effective incentives will need to be tailored to the local context and require the right enabling condition – which include factors such as trust, digital infrastructure, reliable payment systems and levels of financial literacy.

This makes it ever more important for policymakers to explore what incentives work in their local context to increase pension participation in the informal sector. As global populations age and increase the pressure on pension systems it becomes ever more important to engage informal workers if we are to both avoid a future pensions timebomb and reduce the millions of individuals who face old-age poverty without a reliable pension income.

---

Read the full report, written in collaboration with D3P Global

Sign up for news and updates

The Coller Pensions Institute is part of the Jeremy Coller Foundation

Copyright 2025 Coller Pensions Institute. All rights reserved.